Tap. Pay. Go. Tap Cards Are Coming Soon to SRIFCU!

Big things are happening at SRI Federal Credit Union! We’re excited to announce that Tap Cards, also known as contactless payment cards, will soon be available for all SRIFCU Visa® Credit and Debit Cards. This means every member will soon have the ability to simply tap your card to pay, making checkout faster, easier, and more secure.

Why Summer 2025 Is a Smart Time to Buy a Car

Summer is one of the most popular and strategic times to purchase a vehicle. As dealerships gear up for new model releases in the fall, they’re motivated to move current inventory. That means hot deals and promotional pricing are heating up right alongside the weather. Whether you’re in the market for a new or used car, now is a great time to find a vehicle that fits your lifestyle and budget.

Important Updates to Funds Availability and Check Collection Rules

To ensure continued compliance with federal banking regulations, SRI Federal Credit Union would like to inform our members of upcoming changes to Regulation CC, the rule that governs the availability of funds and the collection of checks. These changes, mandated by the Federal Reserve Board and the Consumer Financial Protection Bureau (CFPB), effective as of July 1, 2025.

Important Update: Real ID Requirement for Moffett Field Branch

Starting May 7, 2025, members visiting the Moffett Field branch of SRI Federal Credit Union will need to present Real ID-compliant identification to gain access. This change follows updated entry requirements for NASA Ames Research Center, where the branch is located.

What You Need to Know

Honoring Legacy, Empowering Futures: The 2025 SRI Federal Credit Union Memorial Scholarship

At SRI Federal Credit Union, we’re proud to support education and honor the legacy of those who helped build our credit union community. That’s why we’re excited to announce the 2025 SRI Federal Credit Union Memorial Scholarship — an opportunity for promising students to receive financial support as they take their next big step in life.

How Tariffs Impact the U.S. Market and Why Credit Union Membership Provides Stability

Tariffs have long been a tool used in global trade to influence economic policies, protect domestic industries, and sometimes serve as leverage in international negotiations. However, they can also create volatility in financial markets, affecting everything from stock prices to consumer goods costs. With the ongoing uncertainty surrounding tariffs and their impact on the U.S. economy, having your money in a stable, member-focused institution like SRI Federal Credit Union is more important than ever.

SRI Federal Credit Union: Built to Last, Secured for You

There has been some recent confusion regarding DOGE and the use of the word “Federal” in “SRI Federal Credit Union.” We want to take this opportunity to clarify key facts and reassure our valued members that their financial security remains our top priority.

Kickstart Your Financial Goals for 2025 with SRI Federal Credit Union

The start of a new year is the perfect time to reflect, set goals, and take charge of your finances. At SRI Federal Credit Union, we’re here to help you achieve those goals with products and services designed to make your money work harder for you. Whether you’re saving for a big purchase, paying off debt, or building financial stability, we’ve got you covered.

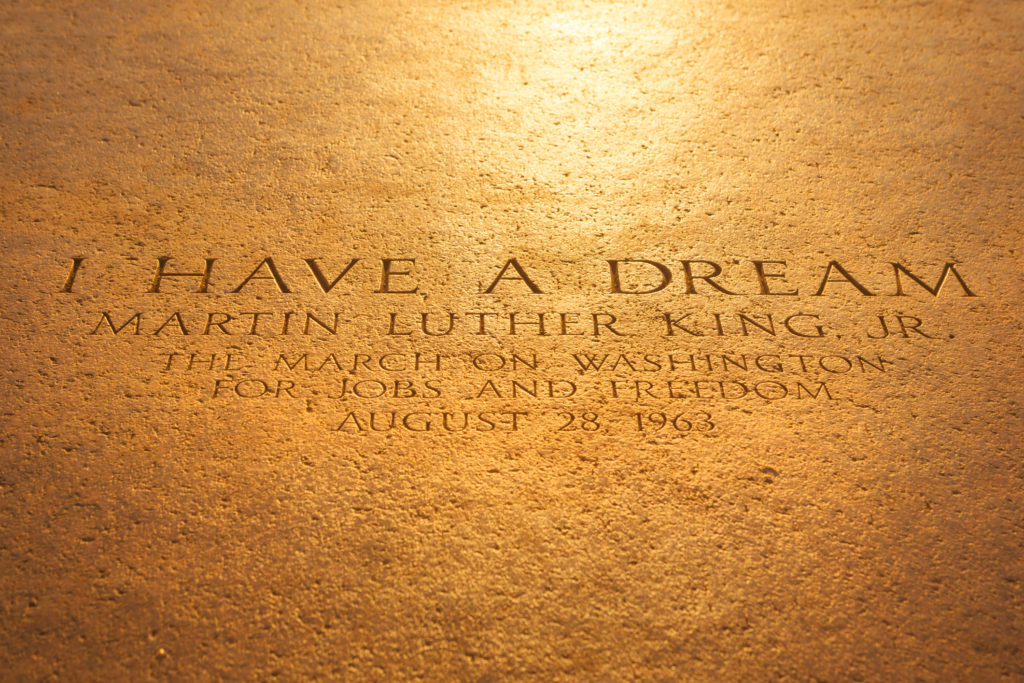

Honoring Martin Luther King Jr.: Financial Empowerment and the Credit Union Movement

As we honor the legacy of Dr. Martin Luther King Jr. this month, we’re reminded of his unwavering commitment to justice, equality, and the empowerment of communities. While Dr. King is most renowned for his leadership in the civil rights movement, his vision extended beyond social equality to include economic empowerment—a principle that aligns closely with the mission of credit unions like SRI Federal Credit Union.

Drive Smarter with SRI Federal Credit Union Auto Loans

Are you thinking about upgrading your ride? Whether you’re eyeing a fuel-efficient commuter car, a family-friendly SUV, or an electric vehicle (EV) to help both the planet and your wallet, SRI Federal Credit Union is here to help you hit the road with confidence. With competitive rates, flexible terms, and a commitment to our members, we’re making it easier than ever to finance your dream vehicle.